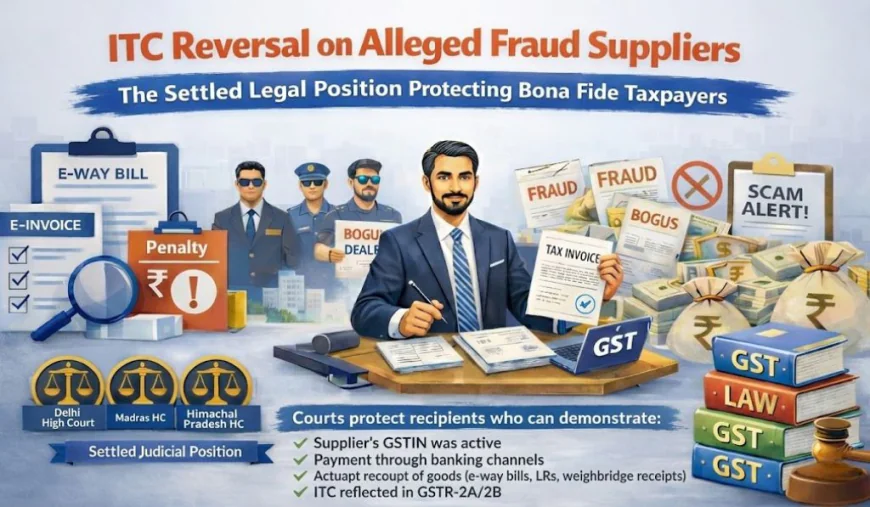

ITC Reversal on Fraud Suppliers: GST Compliance Guide | Mohit S. Shah & Co.

Understand the settled legal position on ITC reversal involving alleged fraud suppliers and how courts protect bona fide taxpayers acting in good faith today.!!

msshahco

msshahco

Input Tax Credit (ITC) is one of the most important features of the Goods and Services Tax (GST) system in India. It allows businesses to reduce their tax liability by claiming credit for the tax paid on purchases used for business purposes. However, one of the most debated compliance issues in recent years is ITC Reversal on Fraud Suppliers. Tax authorities have increasingly scrutinized transactions where suppliers are found to be non-existent, fraudulent, or involved in issuing fake invoices.

Understanding the concept of ITC reversal, the legal framework surrounding it, and the compliance expectations from taxpayers is essential for businesses operating under GST. This article explains the regulatory background, legal interpretations, and practical considerations related to ITC Reversal on Fraud Suppliers.

Understanding Input Tax Credit under GST

Input Tax Credit allows a registered taxpayer to claim credit for the GST paid on goods or services used in the course of business. The primary objective of ITC is to eliminate the cascading effect of taxes and ensure a seamless flow of credit across the supply chain.

Under the GST framework, a taxpayer can claim ITC if certain conditions are satisfied. These conditions generally include:

-

Possession of a valid tax invoice or debit note

-

Receipt of goods or services

-

Tax charged by the supplier has been paid to the government

-

Filing of GST returns by the supplier

-

Proper reflection of the transaction in GST records

If any of these conditions are not fulfilled, the credit claimed may be considered ineligible.

What Is Meant by ITC Reversal on Fraud Suppliers?

The term ITC Reversal on Fraud Suppliers refers to situations where a recipient taxpayer has claimed Input Tax Credit based on invoices issued by suppliers who are later identified as fraudulent, non-existent, or involved in issuing fake invoices without actual supply of goods or services.

Tax authorities may identify such suppliers during investigations or audits. Once the supplier is classified as fraudulent, authorities may question the ITC claimed by recipients who used invoices issued by such suppliers.

In these cases, the tax department may require reversal of the Input Tax Credit claimed by the recipient along with interest or other consequences, depending on the circumstances.

Legal Framework Governing ITC Reversal

The issue of ITC reversal in cases involving fraudulent suppliers is governed primarily by provisions under the Central Goods and Services Tax (CGST) Act, including:

Section 16 – Eligibility and Conditions for ITC

Section 16 of the CGST Act specifies the conditions under which a registered person is entitled to claim Input Tax Credit. One of the important conditions is that the tax charged on the supply must have been actually paid to the government by the supplier.

If the supplier fails to deposit the tax or if the transaction itself is found to be fraudulent, authorities may question the validity of the ITC claimed.

Section 17 – Apportionment of Credit

Section 17 deals with situations where ITC must be restricted or reversed based on the nature of the supply or use of goods and services.

Section 73 and Section 74 – Determination of Tax Liability

If tax authorities believe that ITC has been wrongly availed, they may initiate proceedings under:

-

Section 73 – For cases not involving fraud or wilful misstatement

-

Section 74 – For cases involving fraud, suppression, or misrepresentation

These provisions allow authorities to demand reversal of credit along with interest and penalties where applicable.

Why Authorities Focus on Fraudulent Suppliers

The GST system relies heavily on self-compliance and digital matching of invoices across the supply chain. However, certain fraudulent practices have been identified in the system, including:

-

Issuing invoices without actual supply of goods or services

-

Creating fake GST registrations

-

Passing on fraudulent ITC through fake transactions

-

Circular trading between related entities

Such practices create artificial ITC claims and lead to revenue losses for the government.

To address this issue, tax authorities have implemented analytics-based monitoring systems that track suspicious patterns in GST filings. When fraudulent suppliers are identified, recipients who claimed credit from such entities may also come under scrutiny.

Judicial Perspective on ITC Reversal on Fraud Suppliers

The issue of whether ITC should be denied to a recipient when the supplier commits fraud has been the subject of several judicial decisions. Courts and tribunals have examined whether a bona fide recipient should suffer consequences due to the actions of the supplier.

Some key considerations that courts often examine include:

-

Whether the recipient actually received the goods or services

-

Whether the recipient acted in good faith

-

Whether proper documentation was maintained

-

Whether payment was made through banking channels

-

Whether due diligence was performed before engaging the supplier

In certain cases, courts have held that ITC should not automatically be denied to the recipient if the transaction was genuine and the recipient had no knowledge of the supplier’s fraudulent activity.

However, the final outcome often depends on the facts of each case and the evidence available.

Indicators of Fraudulent Suppliers

Businesses should be aware of potential indicators that may suggest a supplier could be involved in fraudulent activities. Some common warning signs include:

-

Suppliers offering unusually low prices compared to market rates

-

Newly registered suppliers with minimal business history

-

Inconsistent GST return filings

-

Non-availability of physical business premises

-

Frequent changes in business addresses

-

Non-compliance with GST documentation requirements

Identifying these indicators early can help businesses mitigate risks associated with ITC Reversal on Fraud Suppliers.

Importance of Vendor Due Diligence

Given the increasing scrutiny by tax authorities, vendor due diligence has become a critical compliance practice under GST.

Some commonly followed due diligence measures include:

GST Registration Verification

Businesses should verify the GST registration details of suppliers through the official GST portal. This helps confirm that the supplier is legally registered and active.

Monitoring Return Filings

Checking whether suppliers are regularly filing their GST returns can help ensure that the tax collected is being reported to the authorities.

Invoice Reconciliation

Regular reconciliation between purchase records and GST returns (such as GSTR-2B) helps identify mismatches in ITC claims.

Documentation Maintenance

Maintaining proper documentation such as invoices, delivery challans, transport documents, and payment records can help establish the authenticity of transactions.

Consequences of ITC Reversal

If tax authorities determine that ITC has been wrongly claimed due to transactions with fraudulent suppliers, several consequences may arise:

Reversal of Input Tax Credit

The credit previously claimed must be reversed in GST returns.

Interest Liability

Interest may be payable from the date of availing the credit until the date of reversal.

Penalties

In cases involving deliberate misrepresentation or fraud, penalties may be imposed under GST provisions.

Increased Compliance Scrutiny

Businesses involved in such transactions may face increased audits or investigations.

Role of Technology in Preventing Fraud

The GST ecosystem is increasingly leveraging technology to reduce fraudulent practices. Some technological measures include:

-

Invoice matching through GST returns

-

Data analytics for identifying suspicious transactions

-

E-invoice integration

-

E-way bill tracking systems

These systems help authorities monitor supply chains and detect irregularities more effectively.

Best Practices for Businesses

To reduce the risk of ITC disputes related to fraudulent suppliers, businesses often adopt several compliance practices:

-

Conduct periodic vendor verification.

-

Maintain complete documentation for all transactions.

-

Reconcile purchase records with GST returns regularly.

-

Avoid dealing with suppliers with inconsistent compliance records.

-

Ensure payments are made through traceable banking channels.

These practices help create a reliable audit trail and support the legitimacy of ITC claims.

Conclusion

The issue of ITC Reversal on Fraud Suppliers has become an important compliance challenge under the GST regime. As tax authorities continue to strengthen monitoring mechanisms, businesses must remain vigilant about their supplier networks and documentation practices.

Understanding the legal provisions, maintaining strong internal controls, and performing adequate vendor due diligence can significantly reduce the risk of disputes related to ITC claims.

Organizations involved in financial and tax compliance frequently study regulatory updates, judicial decisions, and administrative guidance to better understand evolving interpretations of GST provisions.

Mohit S. Shah & Co.

Office No. 26, 2nd Floor, Anant Building,

217, Shamaldas Gandhi Marg, Princess Street,

Marine Lines (East), Mumbai - 400 002

Phone: + 91-9821462283

Email: officeofmohit@gmail.com